What Is Insurance Bad Faith In NC?

Key Highlights:

“What is insurance bad faith in NC?” is a serious offense that could escalate an otherwise legitimate insurance claim into one of denial, delay, or even undue underpayment.

- In insurance bad faith in NC, insurers commit offenses such as denial, undue delay, low settlement offers, misrepresentation of policy coverage, and improper investigation of valid claims from policyholders.

- The various acts that constitute bad faith include denial, unjustified delay, improper representation, and undue settlement of claims, among others.

- It is possible to prove bad faith on the grounds of legitimate coverage, proper submission of claim, unjustified denial or delay of claim, and lack of proper justification by the insurer for their acts.

- Tatum & Atkinson assist individuals in North Carolina recover contract benefits and compensatory and consequential damages, as well as triple damages under the NC UDTPA Act.

You made sure to pay your premiums on time, and you submitted your claim when the time came. But your insurance company turned you down or even ignored your claim.

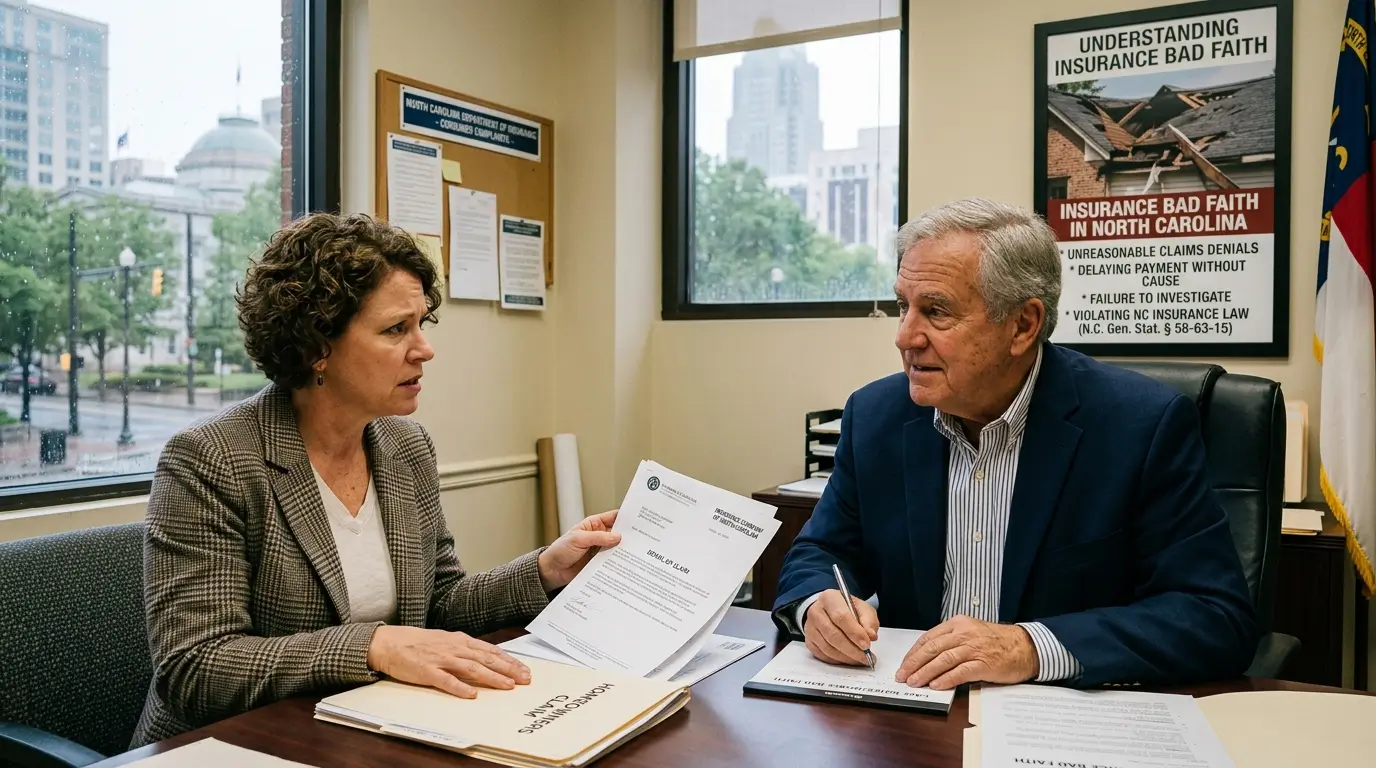

If this is what has happened to you, there is a possibility that you have become involved with an issue the state of North Carolina treats with grave seriousness, insurance bad faith. With this Tatum & Atkinson guide, we will assist you in understanding the specifics regarding what this entails and when it is appropriate for you to take action.

So be ready to know what insurance bad faith in NC is with me, Robert Tatum, lead attorney and co-founder…

What Is Insurance Bad Faith Claim NC?

Insurance bad faith is defined as the unreasonably unfair behavior shown by an insurance firm during the handling of a claim filed by the insured person. Under the insurance bad faith North Carolina laws, the law states that insurers should conduct themselves responsibly and reasonably in relation to their customers who have insurance coverage from them. When there is any denial, delay, or inadequate settlements in an unreasonable manner of claims, the insurer is said to commit bad faith insurance.

Bad faith, therefore, should be noted that a bad experience from a claim is not a case of bad faith. Insurance firms are allowed under the law to carry out investigations, ask for necessary documentation, and even deny certain claims based on justifiable reasons. A case of bad faith can only arise if the insurance company does so without justifiable cause.

A policyholder is entitled to some legal actions in case of a case of insurance bad faith in North Carolina.

Examples of Bad Faith Insurance Practices in NC

North Carolina’s UDTPA and the Unfair Claims Settlement Practices Act specify certain actions that amount to unfair settlement practices within insurance companies in NC. Such actions include unfair insurance settlement practices NC and are not limited to the following:

- Dismissing a claim for an invalid reason: The insurance company refuses to pay on your claim, but cannot cite an exclusion in your insurance policy for the refusal.

- Unnecessary delays in dealing with claims: Delaying and failing to act on claims or responding to communication.

- Settlement offers substantially below the value of a claim: Offering much less than your claim is worth, often without justification.

- Misrepresentation of policy wording: Saying that your insurance does not cover a particular issue when it does, and using only part of a clause.

- Failing to investigate thoroughly: Dismissal of your claim or a refusal to offer payment due to insufficient information.

- Threatening claimants into accepting low settlement offers: Using threats to force someone into accepting a bad settlement deal, often following a car accident.

They manifest themselves in all forms of insurance bad faith lawsuits in North Carolina, whether you have a home insurance bad faith claim North Carolina, an auto insurance lawsuit from being denied an insurance claim, or a bad faith lawsuit against your health insurance.

Wrongful Claim Denials and Delays

There are two of the most prevalent forms of bad faith that are presented to North Carolina policyholders, which are denial and delay. Though related to each other, they present distinct legal issues.

Wrongful Claim Denials

A claim denial that is wrongful occurs when an insurance company wrongfully denies a claim for which it has no justifiable reason under North Carolina law to do so. Examples include:

- Your car insurance claim denied lawyer NC, even though your claim is covered, and there is evidence that you were damaged.

- Your homeowners’ insurance claims due to storms, fires, or water damage are denied based on an excuse created by the insurer after the fact.

- Your health insurance bad faith denial NC is based on classifying the service as “experimental” or “elective.”

In case you have received a denial letter, it should explain what the denial is based on and which policy provision is used.

Unreasonable Delays

Insurance companies have time requirements under North Carolina statutes that they need to adhere to. These include:

- Acknowledging a claim within 10 business days after receiving the notice

- Starting an appropriate investigation immediately after receiving notice

- Confirming or denying coverage for claims within a reasonable period after being provided with proof of the loss

Deliberately delaying is considered insurance bad faith in North Carolina, particularly if there is evidence that the insurance company knows the claim is valid. Delaying causes real-life consequences, like individuals not getting their cars fixed, being unable to afford treatment, and other necessary repairs.

How to Prove Insurance Bad Faith in North Carolina

It is not enough to prove that the insurance company denied claim North Carolina or delayed processing it; you need to prove that:

- You had an existing insurance policy during the time of the loss or incident.

- You made an appropriate claim accompanied by all necessary documentation.

- Your insurance claim was denied or delayed.

- The insurer had no legitimate reason for its actions; alternatively, the insurer knew that its action was baseless but proceeded anyway.

Some pieces of evidence for an insurance bad faith case in North Carolina include:

- The denial letter itself and any policy language quoted.

- Claim files and internal adjuster documents (from discovery).

- Appraisal by another party confirming the true worth of the claim.

- Timeline of all communications proving excessive delay.

- Previous complaints made to the NC NAIC Dept. of Insurance against the insurer.

As insurance companies have possession of the majority of the evidence within their own walls, it is essential to retain a knowledgeable insurance bad faith attorney in North Carolina. An attorney will force the insurance company to turn over their internal documents proving any bad faith denial.

Your Rights Under North Carolina Insurance Law

North Carolina is one of the states that has the best legislative provisions protecting consumers. The following are among the rights provided by the law:

The Unfair and Deceptive Trade Practices Act (UDTPA) — N.C. Gen. Stat. § 75-1.1

This is the most potent piece of legislation used when making claims based on insurance bad faith. It bans any conduct that could be considered an unfair practice. A case decided under this act entitles a consumer to triple damages.

The Unfair Claims Settlement Practices Act — N.C. Gen. Stat. § 58-63-15

The law clearly describes what the insurers are not supposed to do. Although the law is not always used to give an individual a cause of action, it is considered very persuasive for bad faith cases.

The Right to File a Complaint with the NC Department of Insurance

In addition to or even before filing a lawsuit, you have the option to make your complaints on ncdoi.gov. This will put the issue in writing, initiate an investigation by the state, and may sometimes influence the insurer.

One thing is knowing about these rights; enforcing them is quite another. An experienced North Carolina insurance litigation lawyer would be able to evaluate your case against applicable laws and come up with an excellent strategy.

When to File a Bad Faith Insurance Lawsuit in NC

It’s not always the case that an insurance dispute leads to a bad faith insurance lawsuit NC. However, there are certain factors that make it mandatory for you to take the matter to court:

- The reason for denial does not coincide with your policy wording.

- The insurance company hasn’t made a coverage decision for weeks/months now.

- The amount offered by the insurance company is far below what you’ve lost.

- Threats have been made, or the insurance company is pressuring you into accepting their decision.

- A public adjuster/expert has evaluated your case, but the insurance company has decided to ignore their report.

- The loss has happened due to no fault of yours, yet the insurance company blames you for it.

The statutory period for filing claims of insurance bad faith under the UDTPA in North Carolina is four years from the date of the wrongful conduct. But don’t wait. It’s in your best interest to get help early. If anything seems fishy about how you’re being treated by your insurance company, call an attorney right away.

At Tatum & Atkinson, our consultations are free for North Carolina insurance clients. Give us a call at (800) 529-0804, and there’s no fee if you win your case.

Compensation Available in Bad Faith Claims

The key difference between a claim in bad faith and one for breach of an insurance contract is you’ll get paid a significantly higher amount.

Whereas in the average claim case, you’re essentially looking to recoup what you lost based on the policy terms. But in your North Carolina insurance bad-faith lawsuit, you can claim the following:

- The remedies available in the original contract.

- Compensatory damages for any financial loss that was incurred due to the delay (e.g., expenses incurred for treating injuries, extra repair work at home, loss of earnings).

- Three times the damages in the event the insurer behaved willfully and/or recklessly (under the UDTPA).

- Costs of the attorney’s fees and more legal costs.

- Punitive damages in case of grossly negligent conduct by the insurance company.

This is why insurance bad faith cases in North Carolina are worth pursuing seriously. The insurer’s misconduct doesn’t just entitle you to what they already owed you; it can expose them to significantly greater liability.

Why Do I Need a Lawyer for an Insurance Denial?

You don’t necessarily need to retain an attorney for help with a denial by your insurance company. The truth is that insurance companies have whole departments of adjusters and attorneys who try to reduce the payments that they make on claims. Fighting back against this type of opposition on your own, especially during a time of trauma, injury, or loss, is like being outmanned and outgunned.

An insurance bad faith lawyer North Carolina can:

- Look at your insurance coverage and note areas where the insurer might be underwriting the wrong information.

- Make sure you have a legal demand letter that is more powerful than a customer complaint.

- Get hold of the internal claims file using the litigation process.

- Assess all your damages, direct and consequential.

- Go into the negotiation process strong or bring your case to trial.

Ready to Fight Back? Tatum & Atkinson Can Help.

Insurers rely on the ignorance of policyholders about their rights to get away with these injustices since the insured parties either do not know what their rights are or are too intimidated to pursue their case.

Our experienced North Carolina insurance dispute attorneys from Tatum & Atkinson can help you pursue your claim against any insurer that has acted wrongfully towards you in the state of North Carolina, whether it pertains to automobile insurance, homeowners’ insurance, health insurance, or other types of insurance claims or disputes.

- Free consultation, absolutely free of charge.

- Contingency fee arrangement, meaning that you don’t pay anything unless we win your case.

- Expert attorneys in North Carolina available for a free assessment of your case right away.

Contact us at once: (800) 529-0804

There is no time to waste, especially if your claim was rejected or underpaid. We will have a closer look and give you our evaluation of your case.

FAQs: What Is Insurance Bad Faith In NC?

Can I sue my insurance company for denying my claim?

Yes, but not all denials are grounds for a lawsuit. In cases where you feel that there was wrongdoing on the part of your insurance company in denying your claim, such as bad faith practices, fraud, or misconduct, you have the right to take the company to court.

What should I do if my insurance claim is denied?

You should first start by reading the denial letter carefully, comparing it with the policy language. Collect all the relevant documents for making the claim, file a complaint with the North Carolina Department of Insurance, if required, and seek help from a personal injury lawyer before you sign anything.

Is it illegal for insurance companies to delay payment?

Yes. In North Carolina, the insurer is supposed to acknowledge the insurance claim within 10 days and process it in a timely manner. It can be considered unreasonable if the processing of the claim takes too long or if the insurer tries to avoid their responsibility.

How much is an insurance bad faith case worth?

It will depend on the facts of each individual situation. In any event, you may be entitled to whatever the insurance company would have paid according to their policy. If bad faith is established in North Carolina, you will be able to triple your damages for fraud under the UDTPA.

What are my rights against an insurance company in NC?

As per the North Carolina law, some important rights you have include timely, reasonable claims investigation and denial of coverage, along with an explanation of reasons from the policy. You can make a complaint to the NC Insurance Department, and you may also file a lawsuit alleging insurance bad faith as per UDTPA with treble damages.

How long do insurance companies have to respond in North Carolina?

According to N.C. Gen. Stat. § 58-63-15, insurance companies are required to confirm claim receipt within ten days of submission, after which they have thirty days to make an informed decision, subject to any additional complexity.